Quick Hits

- Stocks Rally in November

S. stocks rose on rising investor optimism for faster growth ahead. - Bonds Rebound as Federal Reserve Cuts Rates

Falling interest rates supported bonds during the month. - Supportive Economic Backdrop

The economic updates released in November showed signs of economic growth. - Risks to Monitor

Markets face a number of risks as we finish out the year. - Positive Outlook Ahead

We believe the most likely path forward is for continued market appreciation and economic growth.

Stocks Rally in November

November was a strong month for equities, as investors poured into U.S. stocks following Donald Trump’s election victory early in the month. The S&P 500 gained 5.87 percent in November while the Dow Jones Industrial Average was up 7.74 percent. The Nasdaq Composite finished the month up 6.29 percent after a late-month rally for technology companies. All three indices set record highs during the month, highlighting rising investor optimism for faster growth ahead.

The strong results were supported by improving fundamentals. Per Bloomberg Intelligence, as of November 29 with 97 percent of companies having reported earnings, the average earnings growth rate for the S&P 500 in the third quarter was 9 percent. This is more than double analyst estimates at the start of earnings season for a more modest 4.2 percent increase. This encouraging result is a good sign for investors, as ultimately fundamentals drive long-term performance.

Technical factors also supported U.S. stocks. All three major indices spent the entire month well above their respective 200-day moving averages. (The 200-day moving average is a widely monitored technical signal, as prolonged breaks above or below this level can indicate shifting investor sentiment for an index.) All three of these indices have spent the entire year above their respective trendlines, indicating continued solid investor support for U.S. stocks.

While it was an encouraging month for U.S. investors, the story was different internationally. Both developed and emerging markets fell during the month due to rising investor concerns about a stronger dollar and increased trade restrictions under the incoming administration. The MSCI EAFE Index fell 0.57 percent during the month while the MSCI Emerging Markets Index lost 3.58 percent. Technicals were challenging for international stocks as both MSCI indices ended the month below their respective 200-day moving averages. This marked the second consecutive month that the developed market index finished below trend, potentially signaling rising investor concerns for developed international stocks.

Bonds Rebound as Federal Reserve Cuts Rates

Bonds were up during the month, supported by falling interest rates. The 10-year Treasury yield was volatile during the month; however, it ended November at 4.18 percent, down from 4.37 percent at the start of the month. The Bloomberg Aggregate Bond Index gained 1.06 percent in November.

The Federal Reserve cut the federal funds rate by 25 basis points at its November meeting, which was widely expected by investors and economists. Looking forward, the pace of rate cuts is set to slow, with futures markets pulling back on rate cut expectations modestly in November and pricing in a total of just three additional cuts by the end of 2025.

Even high-yield bonds, which are typically less driven by interest rate movements, were up for the month. The Bloomberg U.S. Corporate High Yield Bond Index gained 1.15 percent in November. High-yield credit spreads fell from 2.88 percent at the end of October to 2.69 percent at the end of November. Tighter credit spreads indicate increased investor appetite for high-yield investments and drove the gains during the month.

Supportive Economic Backdrop

While the election was the major story in November, the economic fundamentals also showed signs of solid improvement during the month. Consumer spending remained impressively resilient despite headwinds from rough weather and higher interest rates. Personal spending and retail sales growth remained healthy in October, which is a good sign for overall economic growth given the importance of consumer spending for the economy.

Additionally, consumer confidence improved notably as well in November. Improving consumer views on both current conditions and future expectations helped push the Conference Board Consumer Confidence index to a one-year high. Historically, higher levels of confidence have supported faster spending growth, so this was another welcome development.

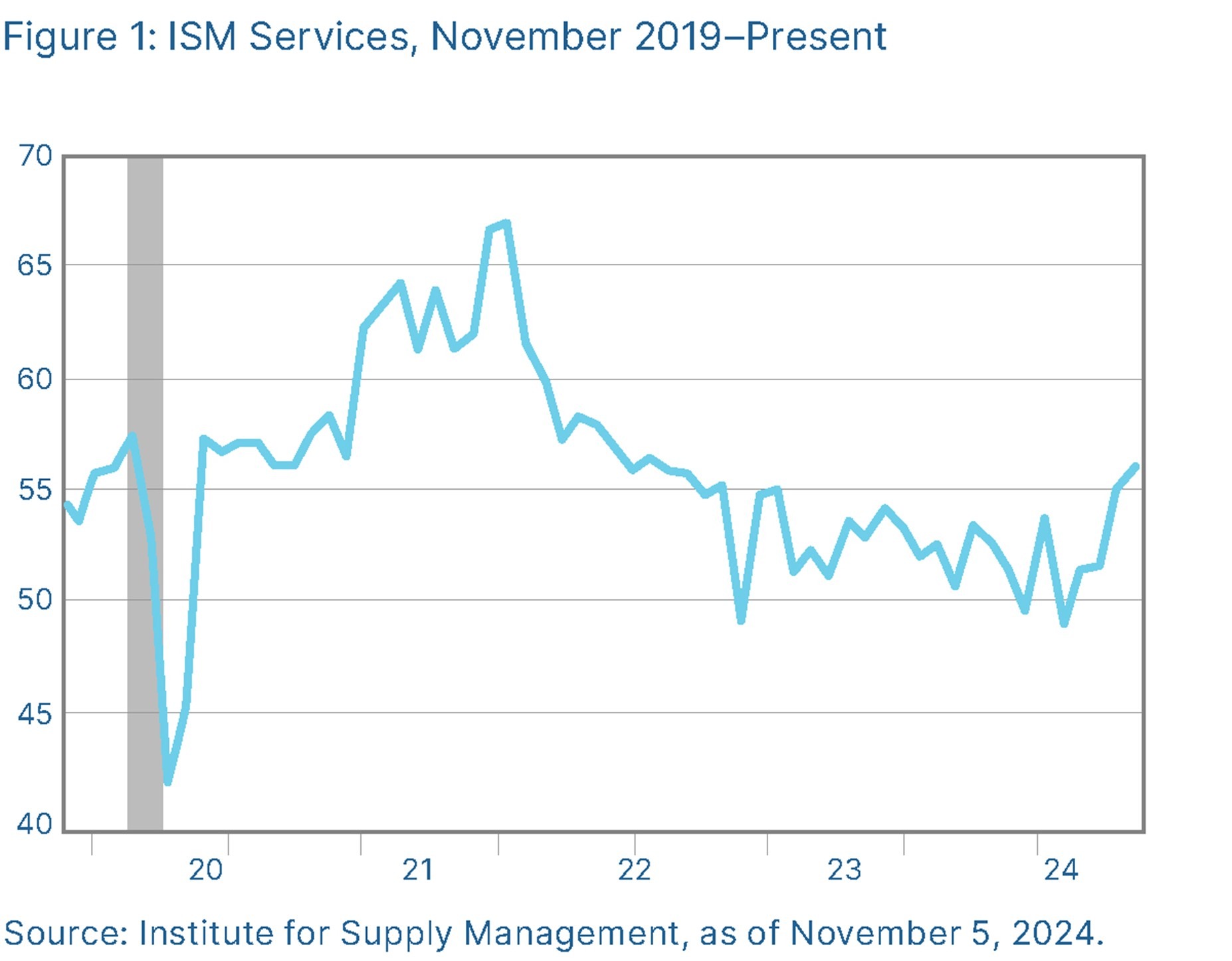

Business spending and confidence also showed signs of improvement during the month. Headline and core durable goods orders rose in October, while service sector confidence rose to a two-year high in November. As shown in Figure 1, service sector confidence has improved notably since bottoming out in June. Given that the service sector accounts for the majority of business activity in the country, this improvement was a good sign for future business spending growth.

The Takeaway

- The economic data releases in November showed signs of continued economic growth.

- Consumer spending growth was strong during the month.

- Consumer and service sector confidence improved in November.

Risks to Monitor

While the solid economic and market fundamentals were welcome during the month, there are real risks that should be monitored. Domestically, we continue to face political uncertainty as we wait to gain more clarity on the incoming administration’s policies and priorities in the weeks and months ahead. Economists and investors will be keeping an especially close eye on any potential changes to tax policy, as tariffs and income tax cuts were key planks of the Republican platform during the campaign.

Aside from the U.S., there are multiple foreign risks as well. The ongoing wars in Ukraine and the Middle East continue to drive geopolitical uncertainty, while the slowdown in China remains an economic risk. Although the market impact from these events has largely been muted here in the U.S., we should still keep an eye on them.

The Takeaway

- Political risks remain top of mind.

- International risks should be acknowledged as well.

Positive Outlook Ahead

As we saw in November, market and economic fundamentals remain healthy as we finish out the year. Companies continue to show signs of strong earnings growth while the recent economic updates have also been supportive for markets. The rally in November was a reminder that, on the whole, things remain in a relatively good place for U.S. investors.

While the November results were encouraging, there are risks that investors should monitor in the months ahead. With that being said, we believe the most likely path forward is for continued economic growth and market appreciation. A well-diversified portfolio that matches investor goals and timelines remains the best path forward for most. As always, if concerns remain, you should speak to your financial advisor to review your financial plans.

Disclosures: This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million. One basis point is equal to 1/100th of 1 percent, or 0.01 percent.

Pacific Crest Wealth Planning is located at 11209 Brockway Rd, Suite C-203, Truckee CA 96161 and can be reached at 530-563-5250. John C. Manocchio, CFP®, CRPC® (CA Insurance Lic. #0H73423) is an Investment Adviser Representative with/and offers advisory services through Commonwealth Financial Network®, a Registered Investment Adviser.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2024 Commonwealth Financial Network